Chapter 01

The Reconstruction Finance Corporation

Introduction

This chapter describes a national mission to revive the Reconstruction Finance Corporation (RFC), the federal institution that dragged America out of the depths of the Great Depression and to victory in World War II. The RFC has all but disappeared from popular memory, but its legacy has never been more important. As America faces new crises that threaten its security and democracy, it's time to resurrect the RFC to transform our economy once again.

Almost every highly industrialized country except the United States uses several large public investment and coordination institutions (ICIs) that play the role the RFC did for the U.S. Germany, for example, has large national public investment banks such as KFW, state-owned public banks (landesbanks), and countless local non-profit banks (sparkasse) and cooperative banks whose mission is to invest in local small and medium-sized businesses (SMEs) and farms.1 These public investment institutions are seen as compliments to the private financial sector, responsible for making investments that are too small, slow, or risky for private banks. They also play a role in coordinating structural changes in the economy when needed, reorganizing and upgrading industries that have fallen behind to make them internationally competitive once again. Investment and coordination institutions are a standard piece of every healthy capitalist economy.

The United States has a long history of destroying its public investment and coordination institutions, only to scramble to restore them when they are needed in a crisis. State-owned public banks and the public Bank of the United States aided in the development of large infrastructure projects in the early republic.2 ICIs played a role in early advances in mass manufacturing, which put the U.S. on a trajectory for global industrial dominance. Over time, however, private bankers succeeded in convincing state legislatures to dismantle state banks, which they viewed as unfair competitors. At the national level, the Bank of the United States became one of the biggest symbols of the conflict between the two primary factions of American politics. The bank was created, dismantled, recreated, and finally dismantled again, leaving the United States without a national currency until after the Civil War.3 During the high-growth Civil War period and the explosive growth of the Gilded Age, the federal government pumped vast amounts of public capital into the private industrial economy through war spending and a system of public land grants that gave out enormous quantities of free capital to industrial startups and incumbents.4 However, the lack of ICIs during this period meant that its growth left large parts of the country behind and was characterized by chaos, waste, corruption, and a sharp rise in inequality, setting the stage for the Great Depression.

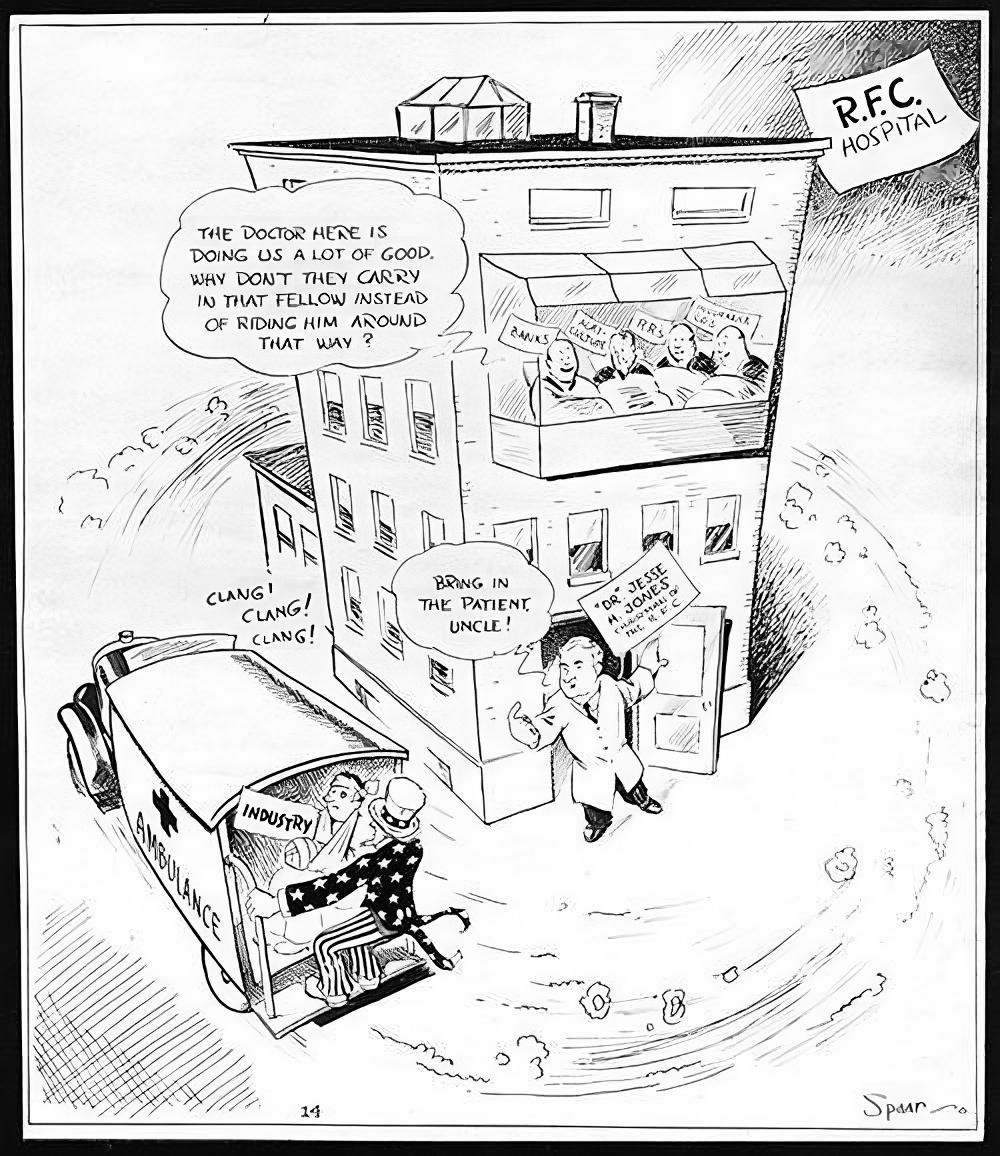

The United States would not have another truly national ICI until the Reconstruction Finance Corporation. The Reconstruction Finance Corporation was created in 1932 by President Herbert Hoover to respond to the Great Depression and was later greatly expanded by Franklin Roosevelt.5 The RFC played a central role in renewing the American economy by providing both financing and coordination for projects large and small, spanning every sector of the economy. It was a publicly-owned corporation, created with an initial grant from Congress of up to $2 billion in capital.6 It quickly became the largest corporation in the world in terms of outlays and income, and it earned a profit for the U.S. government every year of its existence as it grew and upgraded U.S. industry and infrastructure from coast to coast.7 It was the embodiment and the proof of the idea that a national economy is not a zero-sum system.

The RFC's primary role was to make things happen that the private sector was unable or unwilling to - either because they were not immediately profitable enough, they were too risky, or simply due to a general lack of confidence in the future among private investors. When the attack on Pearl Harbor threw America

into World War II, the RFC took the lead in financing and coordinating the wartime economic mobilization.8 The RFC not only solved America's dual crises of war and economic decline but also laid the groundwork for an era of unprecedented domestic stability and economic growth.

The Reconstruction Finance Corporation is the core institution that makes the Mission for America possible. In most other industrialized countries its role would be played by a collection of pre-existing institutions. That we have to create a new institution from scratch comes with both advantages and disadvantages. The primary advantage being that the institution can be created with a built-in culture of urgency and will not be bogged down by decades of accumulated bureaucracy.

The Mission for America is a plan for a president to lead a sweeping mobilization of communities, workers, businesses, and state and local governments to resolve the dual climate-economic crisis together. The Mission for America comprises many separate but mutually reinforcing national missions, each focusing on its own sector of the economy. The national missions build industries and infrastructure that will compose a new clean economy, creating tens of millions of new high-wage jobs along the way and significantly increasing general profitability and national income. Examples of national missions include creating a 100% clean energy grid, transitioning the entire U.S. auto industry to EVs, building a hydrogen industry, building millions of green homes, and much more.

Each national mission will be led by its own dedicated team at the RFC. Federal agencies, state and local government, and the private sector will also play major roles, but the RFC team is charged with the responsibility of accomplishing the mission. That means that the RFC team will make up for any shortfall in private financing, provide leadership, investment, and direct payment for performance and product to engage the private sector and coax competitors to work together when necessary. It will even make venture investments in startups and launch new companies as needed to fill gaps left by private investors.

What unites each national mission is that they can only be accomplished through intense levels of real investment in the American economy for a sustained period. Real investment mobilizes money and labor to create physical products and services that change the material world.9 For example, building a clean power grid will require enormous real investment in clean energy generation to produce electricity, batteries to store it, long-distance transmission to move it across the nation, and substations to distribute the electricity to homes and businesses. Every step of that process requires countless smaller technologies and services to be built, distributed, and deployed.

Unfortunately, the private sector is unwilling to make these investments on its own. Private capital inherently favors low-risk and/or high-reward investments. Decades of American cultural norms and legal precedents have prioritized the short-term whims of shareholders above all other economic considerations. The federal government has only encouraged this bad behavior by dismantling its incentives for long-term real investment and legalizing an array of new speculative financial practices.10 Unfortunately, many of the investments needed to maintain and continually upgrade a national economy are low reward and often high risk. Some required investments are, in addition, enormous. Amid two existential crises of its own making, the American private economy does not have the wherewithal to save itself.

The only way to compensate for the private sector's inability to invest in ambitious nation-building projects is through the use of investment and coordination institutions such as the RFC. Currently, the U.S. does have some small industry-specific programs that resemble ICIs. For example, the Department of Energy Loan Programs Office (LPO) provides financing for many clean energy and manufacturing projects.11 Another example is the Small Business Administration, itself a spin-off from the original RFC, which offers a variety of loans to small businesses of all kinds.12 These programs are important and have a long track record of success. They are, however, limited in their scope. America's existing ICIs lack the heft to make wholesale changes and upgrades to the economy. Under the Biden administration, the LPO received up to $412 billion in lending authority - the first attempt since World War II to provide loans at an adequate scale.13 It was a promising step: proof that a government lending institution could catalyze major investments. But the LPO's future is now uncertain, and even at its peak it did not have the staff or authority to go beyond responding to loan requests to operating on the scale of transforming entire industries.14

The new RFC must be equipped with a wide range of tools to accomplish its mission. Many of these tools were discussed in the Introduction to the Mission for America and will be expanded upon in greater detail in this chapter. However, it must be clear that the RFC is not merely a bank whose sole purpose is to provide loans and loan guarantees. The RFC will provide companies with loans and guarantees when appropriate, but its capabilities go far beyond that. The RFC will be empowered to take equity stakes in the companies it invests in, acting as a true partner in projects and giving American taxpayers a return on their investments. The RFC will be able to initiate procurement contracts with private companies, which can either be sold to private buyers or be used to build strategic stockpiles. The RFC will even be able to create new spin-off corporations and build Government-Owned Contractor-Operated (GOCO) facilities as the RFC did in World War II.15 Many of these tools will sound alien to some readers - though several have recently been employed by the current administration - but they were all used frequently by the original RFC and are still used by many other capitalist democracies every day.

The RFC's success hinges on it being led by qualified leaders who understand the goals of the Mission for America and have both the experience and credibility in private industry to succeed. Choosing who will lead the RFC and its many teams will be one of the most important decisions that the Mission for America president must make. President Roosevelt understood the magnitude of this decision when he appointed Houston entrepreneur Jesse Jones to lead the RFC in 1932.16 Jones fully agreed with Roosevelt's vision of the RFC, understood the economy as both a public servant and a businessman, and was committed to seeing through every investment made by the RFC. Jones was so involved in the day-to-day operations of the RFC, and the RFC so vital to the American economy, that the phrase "you better see Jesse" became a common refrain when someone in Washington wanted something built.17 Whoever leads the modern RFC must demonstrate a similar level of leadership and acumen.

In this chapter, we will discuss the roots of America's chronic real investment shortfall and the nature of real investment itself. Because many of these ideas will feel unfamiliar or unorthodox, we will cover the arguments for and against the positions we take, providing examples from U.S. history and from other present-day economies in an attempt to show readers that what we are proposing with the RFC is normal, safe, and essential.

Why America needs a Reconstruction Finance Corporation

The following sections of this chapter lay out the "why" of the RFC, after which we give our proposal for resurrecting the RFC and making it an integral part of the U.S. economy, including details of the legislative, political and business strategies for launching the new RFC.

Political leadership and social movements play a key role in driving economic development, particularly industrialization, and in modern societies, political leadership relies largely on investment and coordination institutions (ICIs) to transform and grow economies. Today, the U.S. has only a small handful of weak ICIs. By comparison, most other industrialized nations have well-established networks of large and small ICIs constantly working to modernize and upgrade their national industries and infrastructure. Nations with economic histories and traditions as different as those of Germany, France, Japan, and China all benefit from the work of this type of institution. We argue that ICIs are the difference that allows countries with far fewer resources and other advantages than the U.S. to provide living standards on par or better than the U.S. for their working and middle classes.

The United States has a history of periodically dismantling its ICIs, leaving it without the support necessary for investment when it needs it the most. When economic emergencies arrive, the U.S. then scrambles to rebuild these institutions, usually resulting in the creation of a single, massive entity, such as the Reconstruction Finance Corporation (RFC) which served as the nation's central ICI during the Great Depression and World War II.18 Once again, the establishment of a new central ICI is now essential to provide the stability and coordination required to advance U.S. economic interests and to accomplish the Mission for America. For this purpose, we call for the revival of the RFC.

The U.S. currently possesses some small ICIs, mainly lending programs in government agencies, which play vital roles in various sectors. These institutions contribute significantly to economic development, but their impact is limited by their size and scope. Altogether, they account for a small proportion of the national economy and of the investment and coordination capacity needed.19

In light of the history of major ICIs such as the first two U.S. national banks and the RFC all being cut down in political struggles, we propose an approach that will ensure that even if our modern RFC were disbanded, it would leave behind a resilient network of ICIs to support the American economy over the long term. Under our proposal, the RFC will spin off public corporations for specific purposes as needed, which will function as permanent and independent ICIs. This was done by the original RFC as well, and many of its spin-offs live on today as important public and private corporations and financial institutions. This strategy will create a more robust public financing and coordination infrastructure that can withstand political and economic shifts, ensuring that America remains equipped with the necessary institutions to drive innovation, investment, and growth for years to come.

Investment, financial vs. "real"

Rapidly transitioning to a fully sustainable economy requires an extremely high level of nationally coordinated investment for a sustained period. The conventional wisdom regarding investment, including ideas about the appropriate role of the state in investment, is undergoing a profound transition within U.S. academic and policy circles. Therefore, it is appropriate to begin this chapter by explicitly defining our assumptions about investment in general and in the context of the Mission for America in particular, and about the role that the state must play in coordinating, financing, and driving investment.

In the United States, as the center of the economy has shifted away from industry and toward the financial sector and financial speculation specifically, investment has come to be understood primarily as a financial or monetary process - for example, individuals investing in the stock market or a bank investing in mortgage-backed securities. Investment, in this sense, changes nothing in the physical structure of the economy, but merely rearranges the ownership of money and assets. To accomplish the transition to a sustainable economy, nations must physically dismantle and replace billions of polluting machines and transform entire industries and sectors of the economy. Therefore, financing and coordinating investment in the context of the Mission for America refers to the process of mobilizing labor and resources to transform and build the industries and infrastructure needed to create both prosperity for all and a fully sustainable economy. Our challenge is to move atoms, not money.

Because most of us are personally distant from physical economic processes such as manufacturing or construction, it makes sense to back up for a moment to think about the nature of investment from a physical, as opposed to a financial, perspective - in other words, what happens when families, companies, and societies put time and effort into building new structures, systems, capacities, and technology. For our purposes, we will call this "real" investment.

What is real investment? Although the word "investment" is usually reserved for the domains of business, industry, finance, and economics, the same general process is observed in biological and social systems whenever energy and resources are added or diverted away from routine functions into making improvements or other changes to the structure of an organism or society. In this sense, investment is a phenomenon existing across many domains and can be defined as any process that mobilizes energy and resources over a period of time to make changes to systems that transform their function, presumably in ways that better achieve some set of outcomes. In the context of the Mission for America, the outcomes we're seeking are prosperity for all with true environmental sustainability.

How exactly does real investment work as a physical process in modern economies? Even in the case of a Silicon Valley internet start-up, which might seem purely virtual, an investor's action does change the physical structure of the economy: A new group of people along with new equipment are brought together, and they work to create new software that allows customers to work or play in new ways. Although the software they create primarily exists as information, that information is physical in nature, existing on physical devices, changing the way they operate. The software they create, if successful, makes physical changes across the economy and society. Think, for example, of how software such as email, database systems, or video products change how people interact with each other in the real world, or how supply chain management software changed how goods are transported and warehoused.

When it comes to investments into manufacturing industries and infrastructure, the physical changes to the economy are much more tangible: earth is moved; metals, fuel, and other raw materials are extracted and gathered; new buildings and machines are built; and workers are hired and trained in new skills to work in those buildings and operate those machines. This process then supplies ordinary products more efficiently, or it may even produce a new kind of product that changes how billions of people in the world live and work. The mobile phone and the automobile are good examples.

Making physical changes to the structure of the economy in these sorts of ways is inherently more difficult than simply moving money around, and it's usually perceived to be riskier than pure financial investments such as speculating in implicitly government-backed financial bubbles. Therefore, there is a natural tendency for societies to drift away from making real investment happen in favor of financialization.

Today, in democratic, capitalist societies, the mechanism for mobilizing labor and resources into real investment usually is money, which can come in the shape of cash or credit. Throughout history, however, democratic and capitalist societies, and every other type of society, have used combinations of other modes of mobilization, including social and political mobilization, tradition, recruitment of volunteers, slavery, corvée labor, and more. Even today, the kinds of investments we seek with the Mission for America won't be accomplished using money alone. Successfully making a difficult change to the economy - whether creating a new subway line in a busy city or launching a new automaker - requires not only money but also a compelling vision and leadership passionate and tenacious enough to push through endless obstacles and barriers. Right now, for example, several new electric car and truck startups are struggling to get off the ground despite receiving many billions of dollars in investment capital.20

To reorient a society back from financial speculation to real investment requires disruptive leadership that gets people and businesses out of their short-term perspective and into alignment with a more profound and beneficial long-term reward. Politicians and policymakers have begun again to see a role for the state in providing money to finance investment in industry. The Inflation Reduction Act of 2022 mobilized hundreds of billions of dollars in private investment and created over 400,000 jobs - proof that government incentives can trigger massive real investment.21 But the IRA's key provisions were killed by the One Big Beautiful Bill Act in July 2025, demonstrating that programs built on tax credits alone are politically fragile. Politicians have not yet, however, embraced the other side of the equation: the role of political leaders in providing vision and leadership to break through all the barriers and opposition that inevitably stands in the way of transformational national projects. The changes required by the Mission for America are so disruptive that they will certainly face enormous opposition. Therefore, it is crucial that our leaders understand both sides of their role in mobilizing the labor and resources of the nation. That is why the Mission for America deals with both the financing and coordination of investment as well as the political and social strategies required for economic mobilization.

The Mission for America is, in part, a proposal for getting the state back involved in investment on a massive scale. The Reconstruction Finance Corporation is the primary tool for doing this. This raises the question of how the state, through the RFC and other programs and institutions, will know which investments will be beneficial and which will be wasteful or counterproductive. In other words, how can the state, even with the help of an institution such as the RFC, possibly accomplish something in the private economy that our current arrangement of private investment institutions cannot?

The investment required by the Mission for America

Before discussing how the Reconstruction Finance Corporation can be relied upon to choose beneficial investments, we need to define what type of investments would be beneficial in the context of the Mission for America.

The two-sided goal of the Mission for America is to create an economy that is fully sustainable and that can provide prosperity for all. Its plan to achieve that goal rests in part in building industries that will help supply the global transition to full sustainability. While a significant portion of this project involves transitioning away from fossil fuels, its scope is much broader: rebuilding American industrial capacity, modernizing infrastructure, reviving domestic manufacturing, and creating the industries that will employ millions of workers for decades to come.

Taken as a whole, the Mission for America will require investments that achieve the following and more:

Create new industries or expand existing industries to fill in missing capacity where needed. The U.S. is already attempting this in certain sectors, such as vehicle batteries and semiconductors. As promising as these first steps are, current policies are nowhere near big enough to make the difference that's needed.

Establish new industries to replace those that are disappearing due to their unprofitability or unsustainability. The RFC will work to identify and support the creation and growth of new, fully sustainable industries that are high on the global value chain to ensure that every American can earn a living.

Transform harmful industries, wherever possible, to minimize their environmental impact and promote sustainability. The RFC will provide funding and coordination to help industries upgrade to sustainable technologies and production processes.

Wind down industries that are fundamentally incompatible with a sustainable economy. The RFC will step in when possible to provide capital and coordination to transition these industries toward cleaner alternatives. Dismantling harmful industries in a way that ensures stability and fairness for affected workers and communities is absolutely necessary to reduce the nation's total greenhouse gas emissions in a just way.

Develop new infrastructure across various sectors, including energy, transportation, and communications, to support a sustainable economy. The RFC will play a crucial role in facilitating and financing new infrastructure projects.

Upgrade outdated, polluting, or otherwise harmful infrastructure to meet modern standards of environmental responsibility. The RFC will identify and support the redevelopment of infrastructure projects that need updating.

Launch large-scale "Manhattan projects" to develop innovative technologies that address pressing environmental challenges. The RFC will work with government agencies, academic institutions, and private companies to fund and coordinate the development of breakthrough technologies that can help address environmental issues on a global scale.

Support pure research initiatives not currently covered by either the private sector or the government. The RFC will fill the gaps left by private companies, ensuring that essential research projects receive the funding and resources they need to succeed.

Finance and coordinate efforts for consumers to undertake projects such as electrifying and upgrading homes for energy efficiency. The RFC will provide financial support to homeowners to make environmentally friendly upgrades, reducing energy consumption and lowering greenhouse gas emissions.

Finance and coordinate work to modernize commercial and large residential buildings, improving their energy performance and reducing their environmental impact. The RFC will help fund and guide the necessary renovations, promoting the use of energy-efficient materials and technologies in the process.

Help finance a large-scale national workforce development program. The RFC will collaborate with educational institutions and industry leaders to develop training programs that equip workers with the skills needed to fill the millions of new jobs the Mission for America will create.

Assist farmers in reducing greenhouse gas emissions, soil erosion, and water pollution, while maintaining or increasing agricultural productivity through the adoption of new technology and processes. The RFC can support research, development, and implementation of sustainable farming practices, helping farmers contribute to the nation's environmental goals while maintaining a thriving agricultural sector. The RFC will also take on big food monopolies and free farmers from restrictive, predatory contracts, while providing all Americans with access to healthy, affordable food.

The Mission for America's investment strategy encompasses a wide range of sectors and initiatives, ultimately aiming to comprehensively transform the U.S. economy toward sustainability. This holistic approach will require sweeping coordination and investment on an unprecedented scale. The RFC is designed to be able to handle both requirements.

Why nations and companies let real investment lag

Building new productive industries, upgrading old ones, and making big improvements in national infrastructure require difficult and powerful exertion. Just as it is easier to lie on the couch watching TV than to go outside and exercise, it is easier for a nation to let business continue as usual than to build new industries. Sometimes nations get stuck on the couch.

Intuitively, it's easy to understand why it is more difficult to start, for example, a new electric truck company, or a lithium mine, than to simply move money into an index fund that tracks the stock market; or why it's easier for a corporation to make money through financial speculation rather than investing in risky new products. That's why companies like Google and Apple increasingly use their enormous cash piles to buy and sell bonds rather than invest in new products.22 Making something new in the world that works and that is better than all competitors is difficult simply because of all the things that can go wrong or fail to materialize. Moving money into a financial bubble that the Federal Reserve is helping to grow, however, or buying bonds that are guaranteed to pay a fixed interest rate, is easy.

The economy-wide shift toward easy, short-term financial investments and away from investments in the real economy becomes apparent when analyzing how companies make and spend their money. American corporations receive over five times as much money from purely financial activities than they did in the post-World War II era.24 In total, financial activities make up around 30% of corporate profits in America.25 Companies reinvest this money in further financial activities. Non-financial corporations spend around half of their investable funds on shareholder compensation, such as stock buybacks and dividends.26 On top of direct payouts to shareholders, corporations spend billions of dollars every year on other financial activities, such as trading bonds and even cryptocurrency. All of this has occurred alongside companies slashing their investments in fixed assets and other components of the real economy.

On the level of individual firms, several factors work to prevent companies from making real investments and encourage them to make financial investments. One of those is resistance from shareholders. Shareholder primacy is not merely a social norm - it is enshrined in law, as we will discuss later in this chapter. Shareholders powerfully influence and often inhibit a company's decision-making process, not only because they technically own the company and often include its executives and directors, but because legal frameworks compel corporate leadership to prioritize shareholder returns above all other considerations. Pressure from shareholders is one of the reasons that publicly traded companies are significantly less likely to make long-term investment decisions than private

Most of these actors have a strong natural interest in receiving gains in the form of dividends and stock buybacks in the short run over waiting for long-term gradual increases. This dynamic is intensified when the larger economy is dominated by financial speculation. The temptation to spend on short-term financial instruments is too much to ignore when you have shareholders breathing down your neck.

This phenomenon is referred to as "short-termism," and it is frequently found to be one of the biggest drains on private investment in the U.S.27 The problem is so bad that 80% of CEOs have said they would not make an investment that would fuel 10 years of growth if it meant they missed one quarterly earnings report.28 It is hard to justify patiently waiting for a company's long-term investments to pay off in the form of moderate but consistent earnings increases while the rest of the stock market, real estate, and other speculative assets are going to the moon.

Throughout the history of capitalism, the founding generations of industries often keep real investment high as long as they are in charge. Generally, they are leaders who began with a long-term vision to build something new on a grand scale, and they often retain that long-term orientation throughout their career, much to the chagrin of their shareholders. In the U.S., famous examples include Gilded Age tycoons such as Andrew Carnegie, Jay Gould, J.P. Morgan, and Henry Ford.

Henry Ford so enraged his shareholders by constantly investing the lion's share of profits into his beloved factories that they famously sued him. The resulting judgment helped to establish in U.S. law the principle of "shareholder primacy," which requires corporations in many jurisdictions to be run for the financial benefit of shareholders above all other concerns.29

More recently, Steve Jobs, Jeff Bezos, and other famous tech titans stand out as leaders who openly favored long-term investment over returning earnings to shareholders.30 Mark Zuckerberg has invested tens of billions of dollars in the hope that virtual reality will be the next big thing, and that Facebook can become a leader in that field. Part of the reason shareholders don't like these kinds of big, long-term gambles is that they often fail. And at least up until the time of this writing, Zuckerberg's Metaverse gamble is looking like it will be one that doesn't pay off.31 It is in the nature of building something new, large, and complex that it might not work.

Historically, once the founding generation of an industry passes on, the "bean counters" who take over usually begin returning more earnings to shareholders and operating on a more short-term basis.32 In the United States, now that the government has set a precedent to re-inflate speculative bubbles when they crash and bail out any big companies that fail in those crashes, there is a great incentive to view previously risky investments in asset bubbles as being a safe way to earn high returns. In this environment, it's a wonder that any money flows into relatively risky industrial investments at all.

Because private firms on their own are typically unable to maintain healthy aggregate investment across an entire economy, nations must step in with various policies and actions to ensure it. When they do, however, resistance arises from all directions. Just like the voices in someone's head that try to talk them out of going to the gym on a rainy Saturday morning, countless social and economic factions work to protect the low-investment status quo. Why? Fear of change. The most powerful and influential people in a society are usually doing very well. From their perspective, why fix what's not broken? Politicians are naturally and understandably unlikely to fight for economic change as well. Voters crying out for big and expensive investment projects is an extremely rare event. Voters becoming enraged by news reports of money wasted on a failed investment - or a successful one! - is a very common scenario. So why risk it?

But there are many other specific reasons why various interest groups will oppose a public push for greater real investment. For example, building new domestic industries often means protecting them from foreign competition until they become competitive. That can create higher prices for some businesses and consumers, who therefore have a short-run interest in opposing industrial policy. The Civil War is the quintessential example. Southern planters wanted to trade their cotton with England for cheap, high-quality manufactured goods.33 They wanted to be able to continue the slave economy. The North wanted to put tariffs on imports which would force the South to buy goods from new, often inferior and more expensive Northern industries, while retaliatory tariffs would lower the price of their cotton.34 The Civil War was fought in part to ensure that the U.S. would take the path of industrialization.

During the rise of capitalism and when the world filled with new post-colonial nations, every emerging modern nation was the site of conflict between old elites whose power was based on agriculture and resource extraction and who wanted to keep everything as it was, and those who wanted to take the path of industrialization. In most countries, the old elites won, committing billions to live in poverty.35 Only in countries where some sort of revolution broke the back of the old elite was the path of high-investment industrialization taken. For example, as discussed in the previous chapter, the U.S. occupation forces in Korea and Japan forcibly redistributed the land of the old elites to create extremely equal and entrepreneurial societies in which many families suddenly had a little capital and income with which to start businesses.36 In part, that move is what allowed Japan and South Korea to rapidly industrialize without debilitating friction from an old and corrupt agricultural elite.37 But even then, the governments of both South Korea and Japan had to constantly push and pull their major corporations into agreeing to take big risks. Many of the big global brand names like Mitsubishi and Samsung had to be bribed and coerced into taking on their global roles by strong national leaders.38

Even in states that launch sweeping nationalist industrialization projects, however, when the flames of the movement die down, there is a natural tendency for national governments to ease off their investment agendas. Outside of the context of a national development movement that insists on investment and validates a "developmental mindset" among elites, there is no force powerful enough to get politicians to make disruptive and risky decisions around national investment.39

Another general principle that works against national-scale, long-term investment is that it is difficult to accomplish compared with other things that government money can be spent on. During the COVID crisis, the federal government handed out trillions of dollars to individuals and businesses with no strings attached.40 Some of that money could have been paid in the form of investments that put people and businesses to work, improving their capacities. But how? Even just talking about it would have attracted a lot of political heat, and it would be difficult to devise such a plan under short notice in an emergency. Likewise, in the 2009 financial crisis, some economists with the ear of the president urged him to direct stimulus at least partly toward long-term investment that would increase national wealth and security. In the end, however, the White House directed almost no funds toward long-term investment in favor of "shovel ready projects" such as repaving roads.41 This reason nations neglect investment boils down to "investment is hard." And in normal times, investing tends to find its way to the bottom of the priorities list.

Ideological opposition to the state participating in business investment decisions is another powerful force acting against public investment. Several different kinds of ideological opposition to large-scale, state-led investment are usually in play. Perhaps the two most important are: (1) that state intervention in investment decisions will cause dangerous distortions in an otherwise efficient private marketplace, and (2) that excess investment must necessarily create dangerous levels of inflation. The first objection was dealt with in the previous chapter. The second will be addressed in the following sections.

How can a society know what to invest in?

In their book Concrete Economics, economists Brad Delong and Steven Cohen use the analogy of the human body creating muscle and fat to help readers understand healthy vs. unhealthy patterns of national investment.42

Creating new muscle cells is a very expensive biological process for the body, requiring a lot of energy as well as precious materials which have many other important roles in the body. "Investing" in fat cells, however, requires relatively little energy and fewer nutrients. The body predictably defaults to creating fat cells instead of muscle cells unless the signal of strenuous exercise causes it to build muscle. Delong and Cohen use this analogy to give context to the historical pattern in the U.S. of oscillating between periods of heavy investment in productive areas ("muscle") and periods of over-investment in domestic services and financial speculation ("fat").43 Delong and Cohen prescribe a new industrial policy regime that would roll back some of the incentives for investing in services and speculation and would create incentives for investing in productive activity.

But how can political leaders and the ICIs they direct or influence know exactly what qualifies as an investment in productive activities that will increase the wealth and independence of their nations? The fact is there is no way to draw a fine line between what qualifies and what does not. Economists have tried for centuries unsuccessfully to draw a fine line between productive and unproductive economic activity. The dominant "physiocratic" school of economics in the 1700s believed the only productive activity was farming, where the mysterious power of the sun and soil created new life, and that everything else was just rearranging and reshaping the products of the land.44 Adam Smith challenged the physiocrats by arguing that human labor was the source of all value in economies.45 His definition of value included anything that created, improved, or added to a product or structure in the physical world. Services, entertainment, and many other sectors of economies were not included. Later, when it seemed that industrial capitalism was becoming so automated that it would be difficult to provide full employment, economists such as Keynes advocated against distinguishing between productive and unproductive labor, arguing that nations needed to create and honor mass employment in sectors such as services, entertainment, and the arts.46

All of these schools of economists, however, became tongue-tied and confused when they tried to draw a fine line between productive and unproductive labor. The worker who puts seeds in the ground is clearly a productive farmworker according to the physiocrats. But what about the one who makes and repairs the plows? Factory workers who pour molten steel into molds are creating value, according to Adam Smith, but what about their managers?

For our purposes, we are not concerned with trying to define an abstract division between productive and unproductive labor. The Mission for America is attempting to achieve the practical goal of building an economy that is sustainable and that provides prosperity for all. We are therefore interested in financing and coordinating investments in all activities, industries, and infrastructure that can help achieve that goal. The investments we need to reach the goal will span the full range of types of economic activity, including "unproductive" services, pure research, design, engineering, as well as bricks-and-mortar infrastructure and manufacturing.

However, after decades of deliberate deindustrialization, neglect of infrastructure, and over-investment in domestic services and financial speculation in the United States, there is no question that the vast majority of our investment must be directed to industry and infrastructure - the kind of investments Adam Smith was concerned with.

What's so special about manufacturing?

For the past forty years, the most influential economists taught our political leaders that manufacturing was an outmoded way of making a living. They preached that, in the age of globalization, manufacturing would migrate to where wages were lowest because anyone could do it. Therefore, a high-tech, well-educated country like the United States must find its future in the kinds of jobs where no one's hands get dirty, such as computer programming, financial analysis, or even customer service.47

The experts believed it was fine to move all our manufacturing to other countries because we would trade our services for their manufactured items. It was a great idea, in theory. In practice, however, we never found a way to produce enough valuable services to exchange for all the goods and services we needed but no longer could provide for ourselves. Many highly paid industrial workers who lost their jobs were forced to take low-paying service jobs in industries such as retail, fast food, health care, and the informal economy.48 Since de-industrialization began, working-class wages have mostly fallen in real terms, and have dramatically fallen when measured against productivity increases across the entire economy - something we'll discuss in more depth later in this chapter.49

"A modern economy is a service economy." We've heard that for so long and from so many respected economists and leaders that it can be difficult to think about this question clearly. It feels self-evident that making things with our hands in factories is the kind of work that belongs to the 19th century.

One remedy is to think about an extreme hypothetical: Imagine if everyone in our society became a barber. Would we be able to survive as a nation that way? Obviously not - but think about exactly why not. We would not be making or doing most of the things we need to live, such as producing food, clothing, and other goods. Moreover, we would not be making or doing anything we could trade with other nations in exchange for the things we need.

In such an economy, we would be totally dependent on workers in other nations to make the things we need to survive. But since workers in other countries won't come to the U.S. to get their hair cut, we would therefore have nothing to trade with them for all the things that they make and that we need.

It is also hypothetically possible for a full-service economy - one that manufactures nothing - to be broadly prosperous, as long as it produced enough tradable services that trading partners valued highly and could employ their whole population in providing those services. Unfortunately, the reality of the U.S. economy is that our exportable services output has never come close to replacing our lost manufacturing output - not in terms of total value and even less in terms of good jobs provided.

A country that, as in our extreme example, spends its work time on nothing other than non-exportable services would not survive a day. But what about the U.S., which still makes a lot of things, just not enough to meet its needs? Because we want and need more things from other countries than they want and need from us, we run a trade deficit every year. That means that when all the trading in both directions between the U.S. and other countries has been tallied at the end of the year, there is an imbalance, in which the value of goods flowing into the country is greater than the value of good flowing out of the country. Since the 1970s, the U.S. trade deficit has grown from billions of dollars to hundreds of billions of dollars, reaching even more than $900 billion in 2022, up from $845 billion in 2021.50

All this is to say that even though the line between non-productive investments and productive investments is blurry, there is a vast and unambiguous area in which to invest in production. For the purposes of the Mission for America, the kind of investment we seek to increase - and to increase on a massive scale - is anything that mobilizes labor, capital, and resources to create, scale, or upgrade enterprises and industries that have the potential to build the wealth of our society. As we have said, that includes making and doing things that are valuable for ourselves, or for other nations, or for both. This is not limited to manufacturing but also includes any non-manufactured but tradable and valuable products (e.g., films, art, software products) and services (e.g., software development, business consulting, design, and engineering). Any industry qualifies, regardless of whether it produces goods or it produces services; however, it must produce goods or services that American would have to buy abroad if those goods or services were unavailable here, and that could be internationally traded for the necessary goods or services we don't produce ourselves.

Additionally, the types of investment we seek to increase include investments into infrastructure that make the rest of the economy and our entire means of making a living more productive. These investments are also mobilizations of labor, capital, and resources to create, scale, and upgrade our physical economy: roads, bridges, power generation and transmission, communications infrastructure, and more.

What happens when a nation fails to make a living?

When nations fail to invest in their means of making a living - in other words all the industry, infrastructure, and other organizations and structures required to make the things people need and want - they get poorer. As discussed above, if a nation doesn't make and do all the things it needs, it must trade with others who do make and do those things. To meet its needs, it must make and do things that, whether consumed or traded, have a total value equal to what it needs. If the nation doesn't make or do enough valuable things to meet its needs, but continues to live as if it did, then it runs a trade deficit. Let's explore the consequences of this situation for a nation such as the United States.

To get our heads around what this means, let's first think about what happens when a family fails to make a living - that is, when its income falls below expenses. Such a family has four options to make ends meet:

Spend their savings

Sell their assets

Borrow

Seek assistance from friends, family, charities, and/or the government

A family that earns less than its expenses for long enough will eventually spend down all its savings, take on debt if it can, and sell everything it can sell, whether that's tools, a car, or even their house. When all else fails, it can seek assistance from others, including government aid programs. Once all those paths are exhausted, then it will have to start reducing its standard of living.

In practice, a family will usually reduce its standard of living before going through those other measures. In the case of nations, however, political leaders tend not to champion cutting government spending (at least when they are the ones in power) or other policies that would reduce living standards.

When a large, rich nation such as the United States makes and earns less than it consumes, it has all those same options as a family except the last one, as there is no one out there to offer charity to the United States. For the past several decades, that is exactly how we have funded our trade deficit: Americans have spent down their savings; families, companies, and every level of government have taken on massive quantities of debt; and we've been selling assets to foreign nationals, companies, and governments, including assets as diverse as luxury real estate, toll roads, and securitized credit card and mortgage debts.51

The way this plays out on a national level looks very different from how it looks to a family, of course. In the case of a nation, the equivalent of selling a car at a dealership or selling knickknacks at a yard sale is called "foreign investment." When foreign investors, corporations, and governments buy property, businesses, stocks, bonds, or any other sort of asset, that is money flowing into the country which ultimately makes its way to help even out the balance of payments between the nation and the rest of the world.

The nation as a whole can take on debt in many different ways, including government borrowing, corporate borrowing through banks or from issuing bonds, and individuals taking out bank loans such as mortgages and spending on credit cards. Foreign entities buying all these kinds of debt is another way that the balance of payments evens out, allowing the nation to run a trade deficit indefinitely.

Families, state and local governments, and companies can all spend down their savings, or surpluses, as a way of making ends meet. When all these types of entities do this in unison over a long period, the nation is impoverished, even if its people's living standard does not necessarily fall. For decades, the U.S. has been spending down its savings. The personal savings rate, defined by the Bureau of Economic Analysis as "Personal saving as a percentage of disposable personal income", is near an all-time low.52 In fact, the personal savings rate is less than half of what it was for much of the 1960's through 1980's. Some of these savings are paid out of the country, for example to foreign debt holders.

The offshoring of American manufacturing is one of the main reasons why working-class wages have been stagnant for decades, but it is ironically also one of the main factors that made this stagnation feel tolerable for some time. Offshoring manufacturing to developing countries is almost always deflationary. Companies move manufacturing to developing countries because labor, land, and capital costs are generally lower in those countries than in the United States. Developing countries also tend to have significantly weaker labor and environmental regulations, allowing companies to save money by underpaying workers and ignoring environmental concerns. Companies use these cost reductions to produce more goods for less money than if they were produced in America.

This arrangement initially blunted the pain Americans felt from declining wages. For a time, Americans could buy more goods even with a stagnant or declining income. Lower prices helped increase consumer spending and GDP, all while giving workers the illusion that their life was getting materially better because they owned more stuff. This arrangement may not have been sustainable in the long run, but its short-term effects were palpable enough for many Americans to tolerate offshoring.

The rise of easily accessible personal credit was another way policymakers and economic elites could obscure wage stagnation and decline in American workers. Most Americans today have either a credit card, an auto loan, or a student loan. Many have all three. Widely used personal credit is often presented as an eternal aspect of the American economy, but it is a very modern occurrence. Most Americans did not own a credit card until the 1980s. Student loans and auto loans have been around for decades, but their use exploded over the last 40 years. Almost all forms of bank lending were heavily regulated and restricted before the late 1970s. It wasn't until the American economy was dealing with high inflation and the beginning of mass offshoring that policymakers made all forms of credit widely available to Americans.

The rise of the credit card in American life demonstrates this process. The earliest modern credit cards were introduced in the 1950s, but very few households used them, and those that did had credit limits that would be considered exceptionally low by modern standards. It was not until the early 1980s that most Americans used credit cards and that higher credit limits became the norm. Although banks pitched credit cards as a way for Americans to pay off big purchases over time, the unfortunate reality is that many Americans rely on them just to get by. Of all major industrial economies, the United States has the highest average credit card debt, at over $6,000.53 In 2023, U.S. credit card debt hit an all-time high, surpassing one trillion dollars for the first time.54 It is abundantly clear that Americans are not using credit cards to finance large purchases but that millions have become reliant on easy credit to finance their day-to-day existence.

One final example of how the United States propped up GDP and national income during deindustrialization was by selling its assets, such as land and buildings, to foreign entities. The amount of U.S. land, buildings, and resources bought by foreign nationals and corporations has substantially increased in the last few decades. Foreign entities hold interests in over 3.5% of all privately held agricultural land in America - roughly 45 million acres - an 85% increase since 2010 alone.55 That may seem small in percentage terms, but those holdings were valued at over $74 billion as of 2021, and the figure has only grown since.56 In other words, even as U.S. assets are sold to foreigners, this represents capital inflows that help us as a nation live beyond our means.

If America's real investment has been so bad, why does it keep getting richer?

One consequence of U.S. failure to invest in manufacturing and other industries that allow us to meet our needs or to trade for what we need is that tens of millions of workers have lost their claim on the profits of American companies. This has eroded or stalled the earning power of a majority of American workers, even as corporate profits have soared and the professional and managerial classes have watched their incomes rise dramatically.

Only workers who produce valuable goods and services, or who can help capture value that others produce, can negotiate for a fair share of the value they create and have that add up to a prosperous living.57 Workers who create or capture less value than they need to live can achieve a living wage only if subsidies are offered. In the United States, federal and state governments provide enormous subsidies to low-wage employers via the earned income tax credit, food stamps, public health insurance programs, and more. As high-value jobs have left the country, such subsidies have played a greater and greater role in helping to sustain American workers' standard of living.

Before deindustrialization began, millions of workers in manufacturing organized to demand high wages and rich benefits. Their pay raises benefited workers, managers, and professionals across the economy by raising the general standard of pay. In the WWII and postwar era of U.S. industrial dominance, the balance of power between labor and capital was far more even than it is today because the U.S. industrial base was so large and integrated that it was difficult for employers to replicate the same levels of efficiency and profitability in other countries.

Contrary to common perception, industry was not primarily enticed to move to other countries by low wages. If it was as simple as that, then industry would rapidly spread across all parts of the world, starting with the lowest-wage nations. But the nations with the lowest wages in the world remain largely unindustrialized. Rather, certain locations in the world followed the lead of already-industrialized nations and invested heavily in their own manufacturing ecosystems until they became competitive internationally in a few niches or broadly across the full range of manufactured goods. Because the U.S. followed a deliberate policy of deindustrialization while allowing its basic infrastructure to atrophy, it increasingly began to make sense for companies not only to move older, low-tech production overseas, but also to plan new, more advanced investments overseas as well.

Many other high-value, productive, non-manufacturing jobs, such as software development, design, or engineering, also allow workers to bargain for high wages. Those types of jobs do not come in the quantities required to employ a nation as large as the United States, and they are beyond the capacity for workers who have no advanced degrees or specialized skill sets, which is the majority of the workforce in the United States. Only manufacturing can provide vast numbers of working-class people with an opportunity to create goods that are valuable enough to pay high wages.58

The result of the loss of millions of manufacturing and other value-adding jobs has been that most people in the U.S. have experienced a powerful, prolonged downward pressure on their real incomes and standard of living. Real wages for the bottom four quintiles of Americans have stayed virtually flat for the past

40 years, often falling for many years in a row.59 Compared with productivity increases, however, real wages have fallen behind dramatically.60

As we have said, part of what made this path viable for American leaders was that import-based consumption brought down the prices for many goods and introduced many new kinds of consumer goods that helped buoy perceived standards of living even as workers' share of the pie decreased. At the same time, many working-class Americans took on debt to pay for not only the new imported gadgets that were becoming essentials of life, but also for the spiraling costs of major expenses like healthcare and education. Although living standards are difficult to measure and compare across decades, there is ample evidence to show that whereas improvements in productivity, technology, science, and healthcare should all have given American workers a massive increase in quality of life, living standards have, in fact, barely held steady. And to maintain them, Americans have had to spend down savings and take on debt.

But the question remains: If it is true that most Americans are worse off than they would have been if we had continued investing in our means of making a living, then why has America's GDP and GDP per capita grown so much over the same time period? The answer is, in a word, inequality. As it turns out, a nation spending down its savings, selling its stuff, taking on mountains of debt, and suppressing the standard of living for most of its people is entirely compatible with its rich people - and its managerial and professional classes - getting much, much richer.

To better understand how these dynamics function in day-to-day life, think of a real estate developer building a luxury condo building in which many of the units are bought by foreign billionaires looking for a safe place to park their money. This is a real phenomenon that has played a small role in driving up prices of real estate in many U.S. cities.61 Although this phenomenon represents an outflow from the U.S. in the ownership of U.S. assets, and though it may contribute to the rising cost of housing, thereby hitting general U.S. living standards, it can enrich many high-income Americans. Not only does the wealthy local real estate developer make a lot of money from these inflated transactions, but so do many other professionals and entrepreneurs involved in making and executing the deals, managing the buildings, managing the companies that service the buildings, and so on.

The same goes for the process of closing a manufacturing plant in the U.S. and opening one in Mexico or China: Not only does the corporation that owns them benefit from exchanging a newer and more efficient plant for an old one, but so do shareholders and all the managers and professionals who facilitate the transfer. Yes, after that kind of transfer is complete, some U.S.-based managers could find themselves out of a job. But overall, for nearly 50 years, the process of spending down U.S. savings, selling our assets abroad, and taking on massive quantities of debt has provided full employment and constantly rising real wages for the professional-managerial class - at least so far.

To be clear, we are not arguing that trade and foreign investment are inherently bad. We are not recommending that foreign investors should be banned from buying American assets. There's nothing wrong with foreign investors buying assets in the U.S. The problem is that capital and ownership of capital have been flowing out of the country for decades in a one-way destruction of American wealth. This imbalance is causing instability in the world economy. It was the root cause of the 2009 financial collapse, and it is fueling instability in U.S. politics - for example, by contributing, as we argued in the introduction, to the rise of xenophobic and racist populism as represented by Donald Trump.62

One of the premises of the Mission for America is that to leave behind four-fifths of the American people is both morally unacceptable and politically unsustainable. America's political system and its traditions give the working class a way to exact revenge for being left behind. Unfortunately, it does not give the working class a way to take over and steer the nation in a good direction. The system we have allows political parties to make proposals for new directions to the people in attempts to be elected. When the American working and middle classes feel they're being left behind, they exact their revenge by voting in increasing numbers for protest candidates who promise destruction. It is our view that if a political party, or a presidential candidate leading a party, offered a constructive plan to restore income and health and a secure place in the economy to the working and middle classes, then that party would be elected. The Mission for America is a plan for the party or candidate who will hopefully emerge to do that.

One common wrong way to think about real investment

One widespread mistaken way of thinking of economic systems has made it extremely difficult for leaders, policymakers, and the public to think clearly about investment in the national context. This is the tendency to understand economies as mechanical systems. Mechanical systems are more or less fixed in their structure. Human economies, however, are comprised of human beings, human organizations, and human societies. They are, therefore, constantly growing and changing in ways that mechanical systems cannot.

In a machine, a given amount of energy must be split among all the functions of the system. If you do more of one thing, you must do less of another. Think of driving a car on a hot summer day: When you blast the air conditioning, you force energy to be diverted from powering the engine to powering the air conditioner.63 With the air conditioning blasting, you won't be able to drive as far on one tank of gas or one charge of your battery.

Seeing economies as mechanical systems leads people to think that they are static, zero-sum systems, like the car in the previous example. This has dire consequences for leaders and policymakers when it comes to thinking about investment. If the economy is a zero-sum system, then every dollar invested in improvements must take away from other needs. Spending a billion on clean power infrastructure, for example, means a billion less for education or health care. Given such a choice, as discussed above, leaders will usually decide against investment.

But economies are not mechanical systems. They are biological and social systems, because they are made up of human beings, and because those humans are connected not in a fixed mechanical structure but in a fluid social structure.

From a certain perspective, a body or an economy can also be thought of as a zero-sum process. A finite amount of energy and nutrients that enters the body must be split between all of the body's different processes. The same can be said of economies in any given moment: Given a fixed set of infrastructure and equipment, and a fixed quantity of labor and energy, an economy is, in fact, a zero-sum system. The difference, however, is that bodies and economies are not fixed, but can change dramatically in how they operate over time, even in a very short time span.

There is a huge amount of slack in living and social systems. Our bodies, for instance, expend lots of energy and resources on undesirable activities: an autoimmune response can attack healthy tissue, and the human mind can conjure a massive stress response just by worrying about things that can't be changed or that don't exist. Moreover, our bodies store energy in fat and muscle cells and can even recycle almost any type of tissue to find the energy and resources needed to function. Economies and societies have similar dynamics of waste, storage, and redundancy. Our bodies and economies can change radically over time in how they use energy and how they function in many other ways given stimuli such as changes in physical activity levels, diet, and other behaviors. Economies are, in fact, far more flexible in the short run than organisms because economies can change their superficial and even fundamental structure in ways that organisms cannot.

Therefore, even given a fixed input of energy and nutrients, bodies and economies can have non-zero-sum outcomes that are either positive or negative depending on what they do with the available energy. In other words, unlike the electric car in our analogy above, we can turn up the air conditioning to max, drive faster, and double our range, all at the same time. Given the exact same inputs, a person or an economy can become less healthy, and another can become healthier, just by behaving differently. What this means for the Mission for America is that we will be able to live better while investing in an upgraded and sustainable means of making a living - just as we are currently living far below our potential, because we are simply not putting our people, capital and resources to use.

It is important to emphasize that with living systems such as an organism or an economy, performance improvement is achieved not by doing less, for example, by "turning down the AC", but by doing more, such as by exercising or investing. People and economies improve by doing difficult physical work and sometimes incurring painful stress. The right kind of stress to the body is healthy. For instance, putting strain on muscles sends a signal that causes the body to "invest" energy and nutrients into building new muscle tissue. Without that activity, the body would store extra energy and nutrients in the form of fat. An economy, on the other hand, improves by doing the hard work of building infrastructure and industry.

The kind of work that nations need to do to improve their economies is usually difficult in many different ways. As with a body, the activities that improve a nation's economy usually require strenuous and hard-to-achieve effort by the nation as a whole. For example, upgrading the national power grid in the U.S. is infamously difficult. Inertia at every level of government and across our entire national energy industry and infrastructure pushes back against any effort to add a new power line to the grid - just as our bodies resist embarking on the expensive process of building muscle tissue.64 In our bodies, muscle-building will commence only once a very strong signal is sent to the muscles, the nervous system, and other systems. It takes great effort and a lot of disruptive activity to send that signal.

Investing in new power lines, and most other necessary improvements to our economy, also requires very disruptive signals that are powerful enough to overcome the political and economic inertia that seeks to block power lines at every turn. What's interesting here is that doing more, spending more - mobilizing more people, capital, and resources as a nation - is what's needed to make our economy more healthy and prosperous. We build our economies to be more productive and prosperous by undertaking great efforts to push through political, social, and economic inertia to add new, more productive processes to our economy.

When pressed, economists usually agree that in any economy, lots of untapped people and resources can always be unleashed by forging new combinations of people and resources, and they know that many economies in history have transformed themselves very quickly to be more productive and efficient. For mainstream economists, however, these examples might as well not exist; they believe that such things can happen only in extreme crises such as a world war. Later in this chapter, we cite examples in history when this has happened, and we explain why we believe it can happen again in the United States during peacetime.

Who currently decides how our nation invests?

For hundreds of years, capitalist societies have oscillated between two visions of how they should manage investment and coordination of the private economy. In one vision, which has been dominant for several decades in the U.S. and most other capitalist economies, there should be as little coordination as possible. Instead, the economy should be allowed to develop organically. In this vision, the role of the state is to establish and enforce guardrails to prevent harm to citizens and the environment, but that's it.

In the other vision, society, using the state, should set a direction for the economy and actively coordinate its development. In this vision, the state plays a more central role in guiding investments and shaping the economy's trajectory. However, it's important to recognize that in societies organized primarily according to the first vision, as ours has been for decades, planning and coordination is happening - but not in a conscious or deliberate way.

In a privately coordinated society, coordination is carried out by asset managers, banks, venture capitalists, and other financial institutions that decide every day where to channel money. These institutions are empowered to decide for the whole society where virtually all of the society's surplus capital, labor, and resources should go. Banks hold trillions in savings deposits. Asset management firms hold trillions more wealth belonging to ordinary people, institutional investors such as pension funds, government, and high-net-worth individuals. Venture capital firms, private equity firms, and hedge funds invest with the capital of the wealthy as well as institutional investors.

How do these private organizations decide where to invest? Generally, depending on their function, such as a venture capitalist vs. a wealth manager, they will look for more or less risky ways of earning returns on their capital. They do this in a decentralized way, generally just looking for places to put the money they're responsible for, though they are guided by trends and groupthink that can often wind up making it look like there is a central planner pulling the strings.

What these decentralized firms can't do, however, is give their nation an entirely new direction by embarking on something like the Mission for America. There is simply no mechanism that would allow them to do that. Despite the fears and fantasies of many on the far sides of the political spectrum, they do not have institutions to allow them to propose and follow through with great plans. Their scattered gatherings and associations serve only to perpetuate their groupthink, which often makes them money but also is the cause of their periodic falls from grace. Sometimes, individual industries or cliques within industries collude to fix prices or to stop competing on innovation. Although this can be very profitable for a time, it also tends to lead to new competitors eventually rising to wipe out the lazy old players.

Therefore, when a great crisis hits, such as the general crisis of economic stagnation that much of the world suffered in the wake of the 2009 financial crash, it is up to society as a whole, usually facilitated by government, to formulate a response. History has very few examples of combinations of corporations or other private interests stepping up to the plate in the absence of leadership by society.

Hence, when nations run into trouble, they tend to switch out of the totally private, decentralized mode of planning over to the public mode. Only in that way can nations chart a long-term vision and mobilize the necessary labor, capital, and resources through investment to accomplish it.

In a capitalist economy like ours, the resources available for investment are represented by money that falls mostly into the following general categories:

Profits from economic activities such as running businesses

Accumulated savings

Lending

Equity sales

Foreign investment

In our society, the people and organizations that control those funds include:

Asset managers (e.g., Blackrock, Fidelity)

Institutional investors (e.g., pension funds, universities, local governments)

Individual big investors

Corporations (e.g., as bond buyers, investors, speculators)

Banks

Venture capital (firms and individuals)

Other financial institutions (e.g., private equity firms and hedge funds)

The general public (e.g., buying shares or bonds)

Government loan and grant programs

Direct government spending

Public venture capital organizations (which barely exist in the U.S. today)

Public banks (which barely exist today in the U.S.)

Private sources of investment capital tend to seek out opportunities with some combinations of high potential returns, speedy returns, and low risk. In certain historical periods, these have included the same kinds of industrial investments that the Mission for America calls for. For example, during the Gilded Age in the United States, the groupthink among private capital held that one of the best bets in the U.S. was to invest in industrial manufacturing, with the aim of catching up to and surpassing Britain. It was the high-tech boom of that era.65 Several developments made this possible, including that the government was massively subsidizing profits through various schemes.66 Then-high-tech industries such as railroads, steel, oil, and chemicals were the vehicles of speculative bubbles in the same way as the stock market is today - a dynamic that generates its own investment capital when the skyrocketing values of speculative assets (e.g., railroad stocks) turn ordinary people into tycoons.67

Unfortunately, the choice of the U.S. business elite in the Gilded Age to lead the way in launching new, large-scale industries is the exception that proves the rule. The bulk of private capital always tends to take the easy and safe road, and it's very unusual for that to be the road of rapid capital-intensive investment in industry.

In other words, in our society today, as in all societies in all eras, we do have a process for making decisions about how surplus capital will be invested. The process we currently use in the United States is unable to make long-term, large-scale investments in certain kinds of ventures and improvements that are critically needed. Understanding the current decision-making process in the allocation of investment capital is crucial for developing new strategies and policies that can help transition to a more sustainable and coordinated economy. The Reconstruction Finance Corporation aims to build upon this understanding and leverage the power of public investment to drive transformative change in the United States.

The arguments against nations coordinating and financing investment

The practice of nations coordinating and financing investment toward deliberate national economic goals has been attacked for decades under the reigning economic orthodoxy. Although that orthodoxy is disintegrating rapidly under various pressures, its arguments still reverberate powerfully across the policy landscape. Therefore, now we'll review the orthodoxy's arguments against state-led large-scale investment, and then discuss our counterarguments.